Every game development studio planning its next title this year is working from the same uncomfortable brief: budgets are up, timelines are tight, and the market that’s supposed to reward that investment has changed shape underneath it.

Newzoo’s 2026 Gaming Report – officially titled the 2026 PC & Console Gaming Report, puts a number on what that feels like from the inside. In the report’s own words, “development costs are rising, and even proven franchises are no longer guaranteed to succeed. The rules that shaped the industry over the past two decades are being rewritten.”

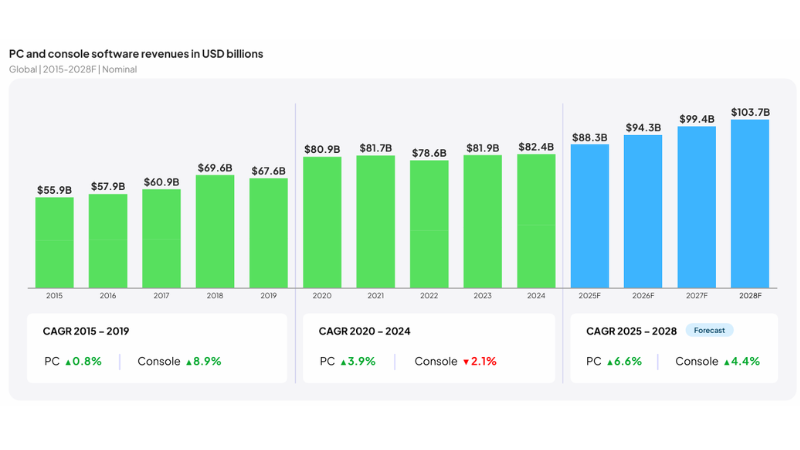

That’s not a marketing headline. It’s a structural read on a market that just came out of a five-year plateau. Global PC and console software revenue is forecast to grow from $88.3B in 2025 to $103.7B by 2028, but the growth isn’t evenly distributed when PC revenue is growing structurally (6.6% CAGR through 2028) and is on track to overtake console revenue outright, while console growth (4.4% CAGR) is being carried almost entirely by hardware cycles and a handful of blockbuster releases rather than genuine player growth.

For a studio deciding what to build next, that distinction matters more than the headline growth number. It tells you where the audience is actually expanding and where it’s just being monetized harder. In GIANTY pov, we read this report the way a production team should, not as market trivia, and we see that Newzoo’s 2026 report seems like a warning label.

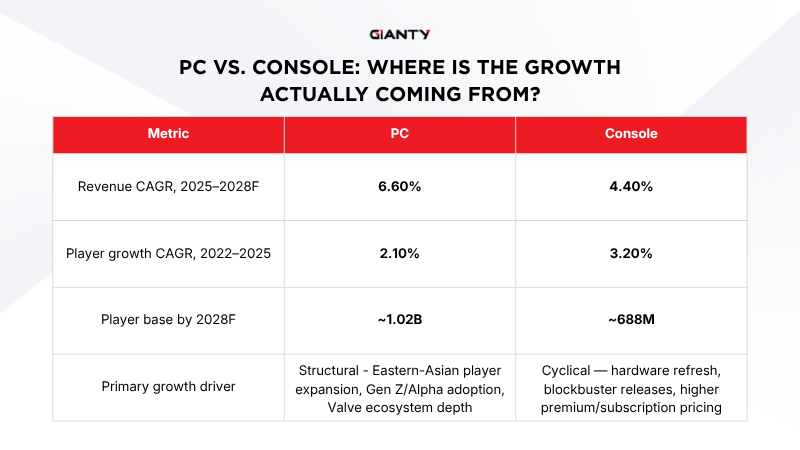

PC vs. Console in Newzoo’s 2026 Gaming Report: Where Is the Growth Actually Coming From?

The distinction is the single most useful data point in the report for a studio’s platform strategy: PC growth is compounding because more people are joining the platform, while console growth is being manufactured by pricing and hit-driven cycles rather than genuine audience expansion. A title designed for console-first monetization is leaning on a market that grows less on its own than PC does.

Is Engagement Growing, Declining, or Stable?

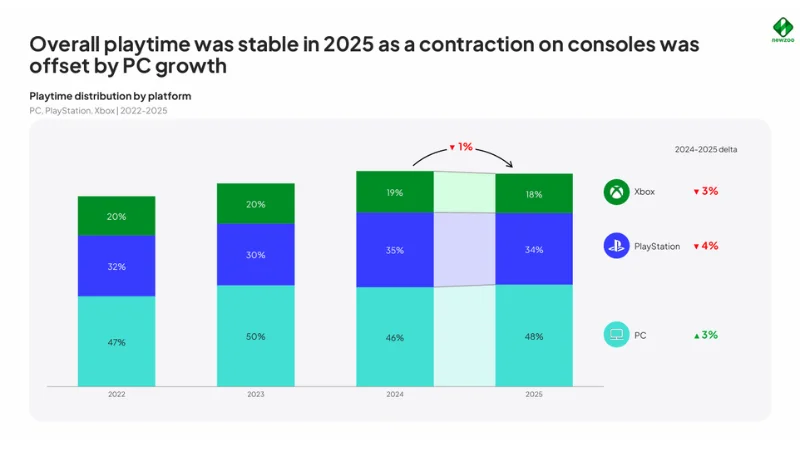

Newzoo’s own chapter summary puts it in one sentence: “Stabilizing engagement has changed the playtime metagame from addition to reallocation.” Top 20 titles still take up more than half of all playtime, but that share is shrinking on every platform and the growing Sandbox share, driven almost entirely by Roblox, still hasn’t fully absorbed the hours lost from AAA-heavy genres like Shooter and Battle Royale.

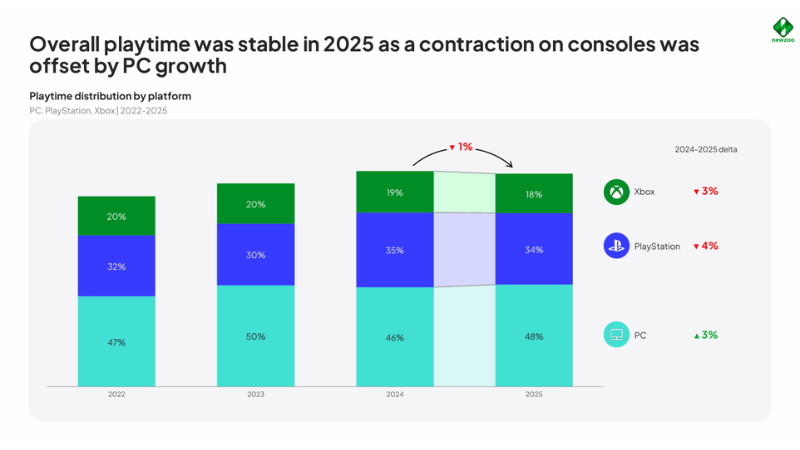

- Global playtime across PC, PlayStation, and Xbox was essentially stable in 2025 — but that stability was a coincidence of offsetting trends, not a sign of a settled market.

- Legacy live-service shooters are losing playtime broadly, even as a handful of fresh entrants post huge growth off a small base.

- Demographically, Sandbox is also the most balanced genre in the market — closer to gender parity than Shooter, Sports, or Battle Royale, and skewing younger, per Newzoo’s Global Gamer Study.

- New-release playtime is stable, engagement is being reallocated, not expanded.

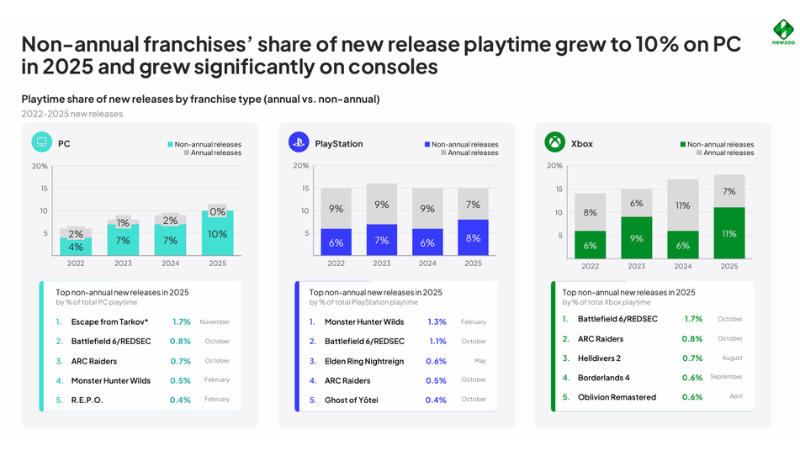

- Non-annual new releases grew from 4%→10% of PC playtime and 16%→30% of PC revenue (2022–2025), outperforming annual franchise releases across PC, PlayStation, and Xbox.

GIANTY’s take: The overlap data here matters as much as the growth numbers, because it’s an audience map, not just a market map. If your title’s genre profile puts it in the Sandbox or narrative-RPG cluster, the data says you’re competing for a different attention pool than the Shooter/Sports/Battle Royale crowd — which changes who you market to, who you cross-promote with, and where a co-op or community feature actually pays off. We use exactly this kind of overlap read when we’re helping a studio decide which systems to prioritize in an RPG or Adventure production: build for the audience that’s actually there, not the audience the genre used to have five years ago.

Why “Bigger Franchise, Bigger Budget” Stopped Being the Safe Bet

Game development has long treated scale as the de-risking move: attach a title to a known IP, put it on an annual cadence, build a live-service roadmap for years of monetization. Newzoo’s 2026 Gaming Report shows that logic breaking down in real time.

- Shooter and Battle Royale, the genres built almost entirely around that scale logic, lost a combined 5 percentage points of playtime share in 2025, despite standout years from Counter-Strike 2 (+22%) and Marvel Rivals (+546%). Battle Royale playtime alone fell 27% year-over-year.

- Call of Duty’s 2025 playtime — combined with new entrants Battlefield 6 and ARC Raiders — still came in below what Call of Duty generated on its own in 2024.

- Annual sports franchises lost 5 points of their own genre’s playtime share in a single year, ceding ground to non-annual titles like Rocket League and new releases like REMATCH and skate.

Meanwhile, the report frames its own standout titles around the opposite quality: “A small, passionate team behind Clair Obscur demonstrates that craftsmanship creates resonance; Schedule 1 shows that cultural timing can be as powerful as production scale.” Both are premium, mid-price, non-annual titles built by teams a fraction of the size of a traditional AAA studio.

GIANTY’s take: This is the pattern we watch most closely on the game development side of our work. The annualized, scale-first model is hitting diminishing returns at exactly the moment its production costs are climbing fastest- studios chasing that model are paying more for a shrinking share of attention. We’ve seen the same shift on the client side: briefs that used to ask for “bigger” now ask for “tighter and better-crafted.”

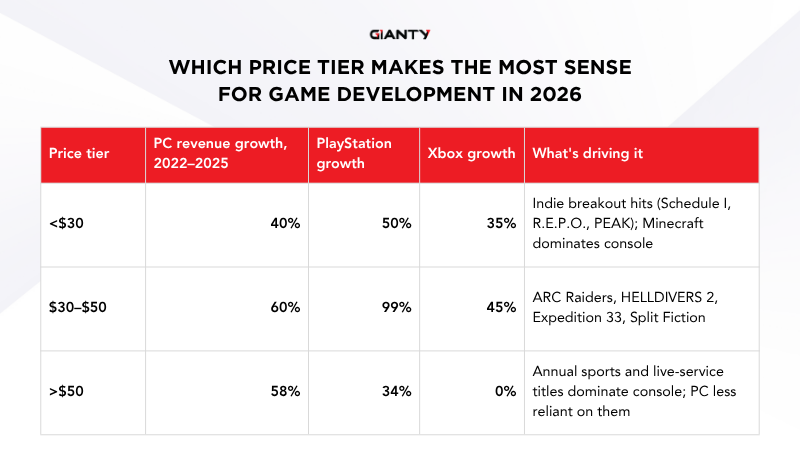

Which Price Tier Makes the Most Sense for Game Development in 2026?

- The $30–$50 tier is the clearest signal in the report: it’s growing faster than both the budget and premium tiers on every platform, and PlayStation’s 99% growth in that band is the single largest movement in the entire pricing dataset.

- For a development team, that reframes the scoping conversation, the goal isn’t “as much game as the budget allows,” it’s the tightest, highest-craft version of the game that fits a price tier the market is actively rewarding.

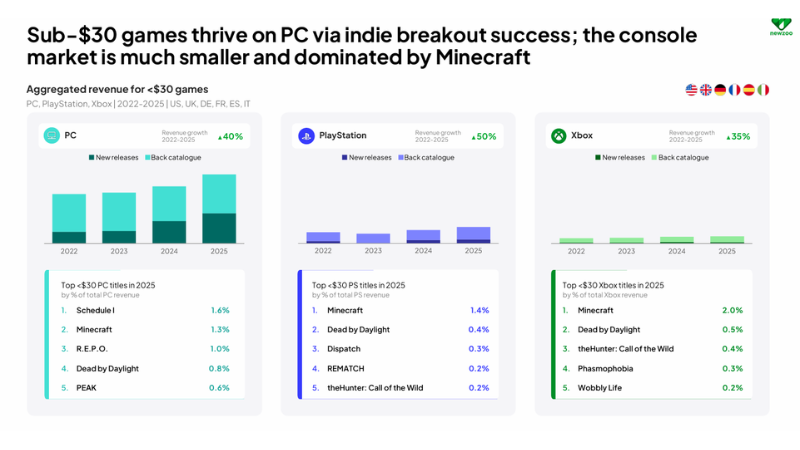

- Sub-$30 success on PC is not a “shovelware wins” story either. Revenue from sub-$30 new releases specifically grew 156% between 2022 and 2025, and the titles leading that growth (Schedule I, R.E.P.O., PEAK) compete on production polish, not just price.

GIANTY’s take: We treat this table as a planning tool, not a trend to react to after the fact. When a studio comes to us mid-scoping, “what price tier is this built for” is one of the first questions we ask because it determines the art density, content cadence, and QA bar the production actually needs, long before it determines the marketing plan.

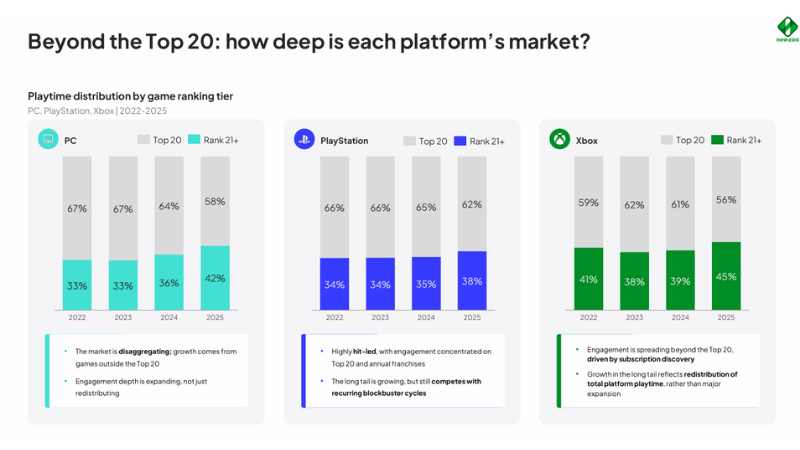

What Happens If You’re Not a Top-20 Game?

- Market concentration remains high across PC, PlayStation, and Xbox, yet the long tail is structurally expanding, most visibly on PC. Survivability beyond the Top 20 depends less on launch-window momentum and more on platform discovery mechanics, catalog depth, and business model fit.

- The same pattern repeats on every platform: long-tail survival is a premium, progression-driven story, not a live-service one.

- In every case, titles outside the Top 20 skew far more toward paid, progression-heavy RPG and Adventure games than the free-to-play, live-service titles that dominate each platform’s Top 20.

GIANTY’s take: “Not Top 20” doesn’t mean “not viable”, well, the data says the opposite. There’s a real, growing, monetizable tier below the biggest hits, and which platform’s long tail fits your title depends on genre and business model, not ambition. A premium, progression-heavy RPG or Adventure title has genuinely good odds in PC’s or PlayStation’s long tail; a title banking on Game Pass discovery to find its audience should design for Xbox’s day-one visibility specifically rather than hoping a launch spike carries it. We factor this platform-by-platform long-tail character into scoping conversations just as much as price tier — where a title launches changes what “surviving past launch” actually requires.

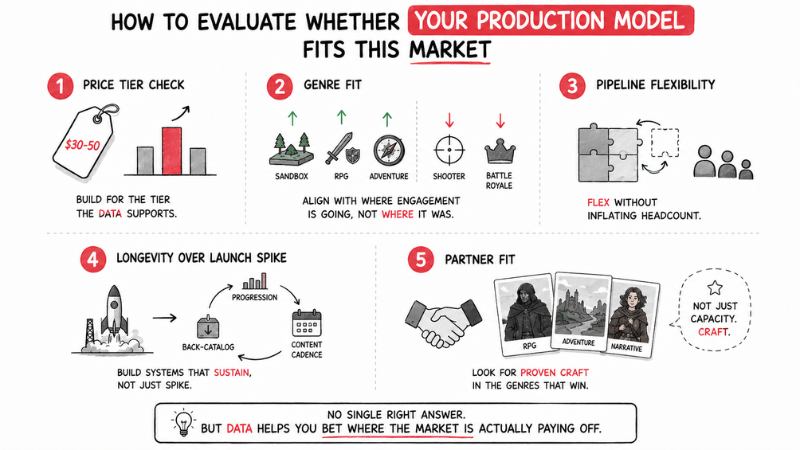

How to Evaluate Whether Your Production Model Fits This Market

Given where Newzoo’s 2026 Gaming Report points the market, a few questions are worth asking of any current or prospective production plan:

- Is your scope built for a price tier the data supports, or for a price tier you assumed you needed? The $30–$50 segment is growing fastest for a reason — it forces disciplined scope.

- Does your genre bet match where engagement is actually going — Sandbox, RPG, and Adventure gaining share — or where it used to be, in Shooter and Battle Royale?

- Can your art and content pipeline flex for those genres without permanently inflating headcount?

- Are you building systems for back-catalog longevity (progression, content cadence) or just for a launch spike that the data shows is increasingly hard to sustain alone?

- If you’re leaning on an external art or co-development partner, do they have a track record in the genres the market is rewarding — not just capacity, but craft in RPG, Adventure, and narrative-driven production specifically?

None of these questions have a single right answer. But Newzoo’s 2026 Gaming Report gives studios something they didn’t have as clearly two years ago: real data on which production bets the market is actually paying off.

What This Means for Game Development Production Capacity

Newzoo’s 2026 Gaming Report points to a direct capacity problem: the games the market is rewarding — mid-price, progression-heavy, art- and content-dense — are also the hardest to build with a fixed internal headcount.

- The mismatch: A shooter on a live-service roadmap can be staffed predictably, one content drop at a time. An RPG, a sandbox title with deep systems, or a narrative Adventure game needs elastic capacity instead — concept art, environment art, character art, and animation work that spikes hard during specific production phases and doesn’t map onto a stable team size.

- Why fixed headcount breaks down: Staffing permanently for peak load wastes budget between spikes. Staffing only for baseline load forces scope cuts exactly when the market is rewarding more content depth, not less.

- The fix: Game co-development and art production partnerships exist to close this gap — flexing capacity up during the genres the market is rewarding, then scaling back down without layoffs on either side.

GIANTY’s take:

- We’ve built for exactly this kind of title for years working alongside Square Enix, contributing to Final Fantasy XV, and shipping 20+ original IPs across the RPG like GOKEN, Adventure, and narrative-driven genres this report shows gaining ground.

- That’s a track record in the same content-intensive production work the data says is winning right now not a capability we’re discovering because the market shifted toward it.

- In practice: an RPG can get a six-month spike in environment art, or a sandbox title can flex its character pipeline from 3 artists to 12 and back again, without the internal team having to break to get there.

FAQs

- What is Newzoo’s 2026 Gaming Report? An annual market analysis of the global PC and console games industry — officially the 2026 PC & Console Gaming Report — covering market trajectory, engagement, market concentration, and business model viability.

- Is video game engagement growing or declining in 2026? Roughly stable overall, but diverging: Newzoo’s 2026 Gaming Report shows PC engagement up +3% in 2025 while PlayStation (-4%) and Xbox (-3%) declined.

- Is PC gaming bigger than console gaming in 2026? Not yet by revenue, but it’s on track to be — Newzoo’s 2026 Gaming Report forecasts PC revenue overtaking console by 2028 (6.6% CAGR vs. 4.4%).

- What price point performs best for game development in 2026? The $30–$50 mid-price tier, per Newzoo’s 2026 Gaming Report — up 60% on PC, 99% on PlayStation, and 45% on Xbox between 2022 and 2025.

- Why did Roblox become the most-played game in 2025? Roblox overtook Fortnite and Call of Duty as the most-played franchise, growing playtime 52% year-over-year and capturing 58% of all Sandbox genre playtime.

- What happens if a game isn’t in the Top 20? It can still thrive: Newzoo’s 2026 Gaming Report shows “long tail” titles ranked 21+ growing playtime 44% on PC, 32% on PlayStation, and 12% on Xbox since 2022.

- Does GIANTY help indie studios apply these game development trends? Yes, GIANTY is a game co-development and art production partner with a track record in RPG, Adventure, and narrative-driven titles and we can help you make your game comes true.